More than $4 trillion in goods are shipped globally each year. The 80% of those goods carried via ocean shipping creates a lot of paperwork. Required trade documentation to process and administer all the goods is approximately one-fifth of the actual physical transportation costs.

Last year, a logistics business and a large technology company developed a joint global trade digitalization platform built using blockchain technology. It will enable them to establish a shared, immutable record of all transactions and provide all disparate partners access to that information at any time. Although the distributed, immutable, encrypted nature of blockchain solutions can help with such business issues, blockchain can achieve much more than that.

Large companies looking to explore new disruptive business opportunities need to think beyond efficiency gains. And to do so, they need real blockchain solutions.

Why blockchain matters to CIOs

Gartner estimates blockchain will generate $3.1 trillion in new business value by 2030, but with the technology set to be ready for more mainstream adoption through 2023, organizations should be exploring the technology now. This is especially the case because large multinational corporations and digital giants are looking to capture larger market shares by implementing blockchain components like specifically distributed ledger technology to reinforce a centralized approach to business.

Consequently, CIOs are under pressure to help guide decisions as to if and how blockchain can be implemented in their enterprises. Organizations that have laid the groundwork to utilize and implement the technology will be in a better position to differentiate and more effectively compete in their markets and regions.

“

Exploiting blockchain will demand that enterprises be willing to embrace decentralization and strategic tokenization in their business models

”

For CIOs, it’s necessary to understand what blockchain is and how it works, and more importantly, how the technology can be utilized to further mission-critical business priorities — or even disrupt the business completely. But only 3% of CIOs have a form of live and operational blockchain for their business, and those solutions that do exist focus mostly on efficiency of existing process versus business disruption and new value creation.

“Blockchain technologies offer a set of capabilities that provide new economic, business and societal paradigms,” says David Furlonger, Distinguished Vice President Analyst, Gartner. “Exploiting blockchain will demand that enterprises be willing to embrace decentralization and strategic tokenization in their business models and processes — even if these strategies are not straightforward.”

Blockchain introduces challenges ranging from strategic issues around how to compete and collaborate at the same time (e.g., in an industry consortium) to the lack of technical interoperability, security issues, and multiple data management and regulatory situations, including addressing various security and privacy laws such as the EU’s Global Data Protection Regulation (GDPR).

What’s the value of blockchain?

Blockchain allows participants who may not know each other to safely and directly do business — in theory without the need for a lawyer, bank, broker or government to mediate the deal.

The blockchain confirms the identity of participants, validates the transactions and ensures that everyone plays by its rules. The wide range of assets that can be traded and participants that can take part — including machines — creates huge commercial possibilities.

For example, once the technology is fully matured and integrated with complementary technologies such as AI and IOT, autonomous agents acting on behalf of a driver could negotiate insurance rates directly with multiple car insurance companies using data from sensors.

What is blockchain?

True blockchain has five elements: Distribution, encryption, immutability, tokenization and decentralization.

Distribution: Blockchain participants are located physically apart from each other and are connected on a network. Each participant operating a full node maintains a complete copy of a ledger that updates with new transactions as they occur.

Encryption: Blockchain uses technologies such as public and private keys to record the data in the blocks securely and semi-anonymously (participants have pseudonyms). The participants can control their identity and other personal information and share only what they need to in a transaction.

Immutability: Completed transactions are cryptographically signed, time-stamped and sequentially added to the ledger. Records cannot be corrupted or otherwise changed unless the participants agree on the need to do so.

Tokenization: Transactions and other interactions in a blockchain involve the secure exchange of value. The value comes in the form of tokens, but can represent anything from financial assets to data to physical assets. Tokens also allow participants to control their personal data, a fundamental driver of blockchain’s business case.

Decentralization: Both network information and the rules for how the network operates are maintained by nodes on the distributed network due to a consensus mechanism. In practice, decentralization means that no single entity controls all the computers or the information or dictates the rules.

Understanding each of the elements, and how they come together to form a true blockchain, gives CIOs a framework to explain the technology to executives and clear up misconceptions. CIOs can also use the elements to explain the difference between partial blockchain-inspired solutions and complete- and enhanced-blockchain solutions.

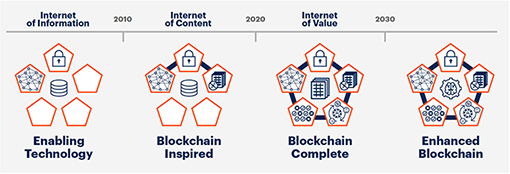

The Gartner Blockchain Spectrum

As the hype around blockchain develops, vendors are flooding the market with promises and solutions mostly focusing on efficiency gains. CIOs must understand the difference between real and partial solutions and invest in those that offer true benefits.

Most early blockchain solutions lack the elements of tokenization and decentralization. Gartner refers to these solutions as “blockchain-inspired” on the Gartner Blockchain Spectrum, which has three phases.

Phase 1: Blockchain-inspired solutions

This phase began in 2012 and will last through the early 2020s. These solutions include only three of the five elements: Distribution, encryption and immutability. Often these offerings are experimental and not fully implemented, and they focus on creating greater efficiency by streamlining existing processes.

Phase 2: Blockchain-complete solutions

Solutions in this phase include all five elements, with the intent of delivering on the full value proposition of blockchain. Currently, only startups are focused on this level of maturity, though Gartner expects these solutions to gain momentum in the market around 2023.

Phase 3: Enhanced-blockchain solutions

The third phase of blockchain will combine blockchain-complete solutions with complementary technologies such as artificial intelligence (AI), the Internet of Things (IoT) and decentralized self-sovereign identity (SSI) solutions.

“Enterprises can easily make missteps that will leave them out of position to capitalize fully on blockchain by being lulled into a false sense of progress and capability,” says Christophe Uzureau, VP Analyst, Gartner. “Shift strategic investments to blockchain-complete solutions and away from blockchain-inspired solutions that reinforce centralized processes and hinder the enterprise from achieving the most business value from blockchain.”

Blockchain crosses industry boundaries

CIOs can begin their exploration by studying blockchain use cases across industries. For supply chain, the initial applications range from the ability to track a mango from farm to store (traceability) or proving the heritage of a genuine object from factory to store (counterfeits) to managing records (efficiency).

Governments have also been exploring potential applications, and although many are still nascent, some interesting use cases have emerged. For example, a Utah county in the U.S. has explored blockchain for its municipal elections. And blockchain solutions are also enabling a higher level of accountability and ability to measure the real impact of policies.

In the financial services industry, blockchain opens up opportunities for cross-border payments, trade finance, securities settlement efficiency and more secure identity systems. But the real transformation will occur with the creation of new digital assets and the decentralization of finance.

Security, technology and legal limitations

As with all technologies, blockchain is not without its challenges. For example, established laws may still need to be revised or put in place to accommodate blockchain use cases, and financial reporting and compliance is still unclear. The technology also lacks legal, tax and accounting frameworks, native interoperability and scalability, and limited or inadequate governance models and standards are currently in place.

Many versions of blockchain are being built within existing operating models, where the original intention was to disrupt and disintermediate centralized entities, operations, processes and business models using open source and democratized engagement.

Further, security for blockchain is a challenge given the lack of best practices and standards, especially when dealing in a consortia context. Within cryptocurrency, for example, tens of millions of dollars have been stranded or stolen due to misunderstandings, basic code errors, fraud and security errors. Security vulnerabilities also exist in the technology that surrounds the blockchain ledger, meaning all blockchain projects must be evaluated for technology, governance and compliance, human misunderstanding and value at risk.

Blockchain as a disruptor

The timing and launch of bitcoin seemed intentionally designed to disrupt the financial and banking industries. However, due to customer mindsets, established and effective solutions, and limiting technology, it seems unlikely to succeed in the way originally intended. In other industries where blockchain could be disruptive, risk-averse companies are keeping a tight hold on the risk factors, resulting in incremental improvements instead of game-changing disruption. The lack of executive understanding is also a critical inhibitor.

These industries include healthcare, supply chain and government. Even traditional disruptors such as Uber and Airbnb could be disrupted by the eventual successful implementation of blockchain. These companies, part of the “peer-to-peer” economy, have created dependence on their digital platforms acting as middlemen.

Companies looking to utilize blockchain technology will be able to remove the central authority figure altogether. Achieving transformative change in this sector will take time due to the usual adoption and technical challenges mentioned above — but the potential for blockchain-complete and enhanced-blockchain solutions is already leading blockchain natives (companies born on the blockchain) to create new and impactful business models.